Here's why wind energy development is likely to peak in 2020

David Wagman | September 13, 2019The U.S. wind market is on track to add 14.6 gigawatts (GW) of generating capacity in 2020, according to consulting firm Wood Mackenzie’s North America wind power outlook.

Phase out of the federal Production Tax Credit (PTC) beginning in 2021 has developers rushing to complete projects in 2020, the report said. In turn, demand is driving bottlenecks in both logistics and grid interconnection requests. As a result, project delays are growing, likely impacting the volume and timing of wind capacity installations.

Logistics bottlenecks are likely as developers rush to take advantage of federal tax breaks for wind. Source: National Renewable Energy LaboratoryAnthony Logan, the report's lead author, said that although the PTC phase-out schedule has been in place since 2015, offtakers were slow to act to procure new capacity. This resulted in relatively subdued installation totals in 2017 and 2018.

Logistics bottlenecks are likely as developers rush to take advantage of federal tax breaks for wind. Source: National Renewable Energy LaboratoryAnthony Logan, the report's lead author, said that although the PTC phase-out schedule has been in place since 2015, offtakers were slow to act to procure new capacity. This resulted in relatively subdued installation totals in 2017 and 2018.

“The lack of available logistical resources will begin to cause schedule rearrangements and delays that will grow more apparent during the first and second quarters of 2020,” he said.

In August, the American Wind Energy Association said that more than 200 wind projects were underway across 33 states. The industry trade group said that 15 of those states had more than 1,000 MW of wind capacity that was expected to come online in the near term. Texas had the most development activity (9,015 MW), followed by Wyoming (4,831 MW), New Mexico (2,774 MW), Iowa (2,623 MW) and South Dakota (2,183 MW).

Federal tax credits

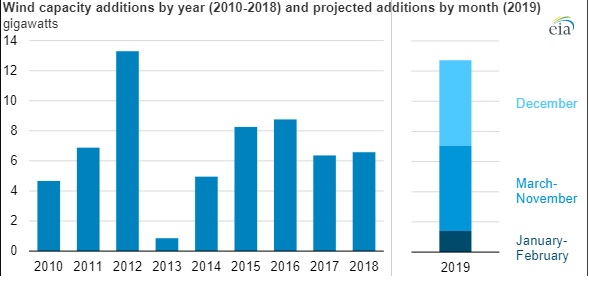

The Energy Department's Energy Information Administration (EIA) said in May that it expected U.S. wind capacity additions in 2019 to total 12.7 GW. That would exceed annual capacity additions for the previous six years, but fall short of the record 13.3 GW of wind capacity added in 2012.

Wind capacity development is expected to peak in 2020. Source: NRELEIA said that changes in annual capacity additions for wind are often explained by changes to tax incentives. The PTC provides operators with a tax credit per kilowatthour (kWh) of renewable electricity generation for the first 10 years a facility is in operation. It was initially set to expire for all eligible technologies at the end of 2012 but was later retroactively renewed.

Wind capacity development is expected to peak in 2020. Source: NRELEIA said that changes in annual capacity additions for wind are often explained by changes to tax incentives. The PTC provides operators with a tax credit per kilowatthour (kWh) of renewable electricity generation for the first 10 years a facility is in operation. It was initially set to expire for all eligible technologies at the end of 2012 but was later retroactively renewed.

The high level of annual capacity additions in 2012 was driven by developers scheduling project completion in time to qualify for the PTC. Similarly, the increase in annual capacity additions for wind scheduled for 2019 is largely driven by the legislated phaseout of the PTC extension for wind.

EIA said that when renewed in 2013, the PTC provided a maximum tax credit for wind generation of 2.3 cents per (kWh for the first 10 years of production. Under the PTC phaseout, the amount of the tax credit decreases by 20 percentage points per year from 2017 through 2019. Facilities that begin construction after Dec. 31, 2019, will not be able to claim the PTC.

Under the current PTC legislation, wind projects are eligible to receive credit based on either the year the project begins operation or the year in which they demonstrate that 5% of total capital cost for the project has been spent and project construction has begun. EIA said that this 5% down method, known as safe harboring, enables wind developers to receive the PTC at a given year’s level, provided they complete construction no more than four calendar years after the calendar year that construction of the facility began.

That means that U.S. wind project developers who want to receive the full 2016 value of the PTC must begin operations by the end of 2020.

Capacity factors

An August report from the Lawrence Berkeley National Laboratory credited increased blade lengths with increased wind project capacity factors, one measure of project performance. The report said that average 2018 capacity factor among projects built from 2014 through 2017 was 42%. That compared to an average of 31% among projects built from 2004 to 2011 and 24% among projects built from 1998 to 2001.

Subdued growth in 2017-2018, then a boom. Source: EIAFavorable wind turbine pricing continues to push down installed project costs, the report said. Wind turbine prices have fallen to $700 to $900/kilowatts (kW). The average installed cost of wind projects in 2018 was $1,470/kW, down 40% since the peak in 2009 and 2010.

Subdued growth in 2017-2018, then a boom. Source: EIAFavorable wind turbine pricing continues to push down installed project costs, the report said. Wind turbine prices have fallen to $700 to $900/kilowatts (kW). The average installed cost of wind projects in 2018 was $1,470/kW, down 40% since the peak in 2009 and 2010.

Wind energy prices also are at historical lows, the report said. After reaching 7¢/kWh for power purchase agreements (PPAs) executed in 2009, the national average price of wind PPAs has dropped to below 2¢/kWh. This nationwide average is dominated by projects located in the lowest-priced regions of the country. At the same time, the laboratory's annual market report said that these prices are due in part to the federal tax credit and compare favorably to the projected future fuel costs of gas-fired generation. Solar PPA prices have "declined precipitously," the report said, pressuring wind’s competitive position.

If not wind, then what?

After the peak, then what? Source: NRELThe Wood Mackenzie forecast assumes that 6.6 GW of projects scheduled for 2020 will not reach connection to the grid until 2021.

After the peak, then what? Source: NRELThe Wood Mackenzie forecast assumes that 6.6 GW of projects scheduled for 2020 will not reach connection to the grid until 2021.

The report also estimates that roughly 1.5 GW of additional capacity will be canceled ahead of project construction. Any affected offtakers likely will choose solar photovoltaic resources to replace the undeveloped wind generation.

Wood Mackenzie said that solar PV benefits from a 30% solar Investment Tax Credit and is beginning to compete "more effectively" with onshore wind on cost. Solar is forecast to maintain a marginal advantage over wind due to a 10% ITC offered to solar PV in perpetuity after the wind PTC phases out.

Although wind will remain competitive in key states through 2021, the negative cost impact associated with the PTC declining to 60% and then 40% of its original value is forecast to outpace cost of electricity reductions in 2022 and 2023.

Wood Mackenzie forecasts the U.S. will add 12.3 GW of wind power in 2021, before falling to roughly 5.9 GW in 2024.

co2 immersions and globel warming

here is why.. didn't read the article but I can answer this question.

it doesn't compete with coal and natural gas.

CO2 is a result of sun caused global warming (not man made)

the only alternative energy to compete with coal and natural gas is Nuclear, and that would be by reducing some of the paperwork restrictions (those that are outdated and not needed).